© ESB Professional / Shutterstock.com

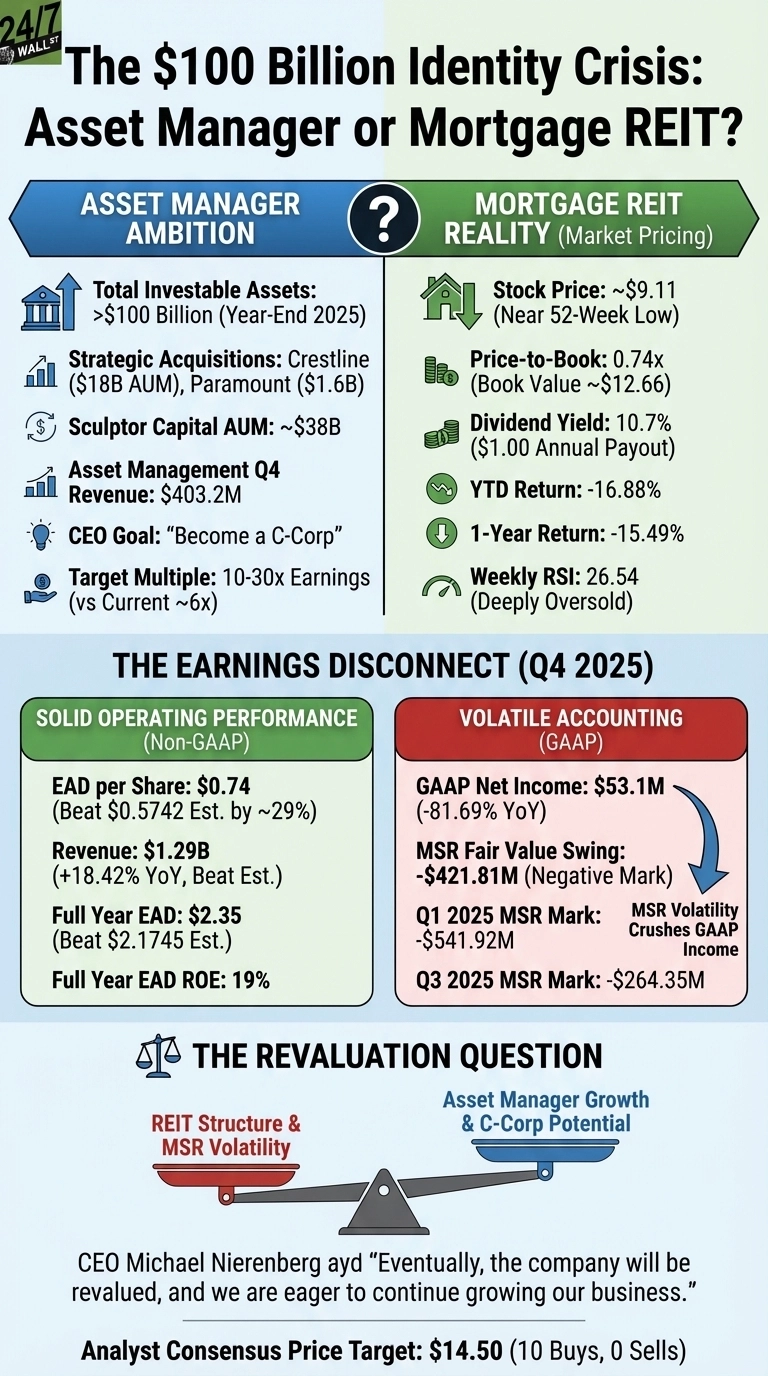

Rithm Capital (NYSE:RITM) just crossed $100 billion in investable assets and posted a blowout quarter, yet the stock sits near its 52-week low. That disconnect is the central question facing investors right now.

The Earnings Picture

Rithm’s Q4 2025 non-GAAP earnings available for distribution (EAD) came in at $0.74 per share, beating the $0.5742 consensus estimate by nearly 29%. Revenue hit $1.29 billion, up 18.42% year-over-year. For the full year, EAD reached $2.35 per share against a $2.1745 estimate, and the company delivered a 19% EAD return on equity.

GAAP told a different story. A $421.81 million negative swing in mortgage servicing rights (MSR) fair value crushed GAAP net income to $53.1 million, down 81.69% year-over-year. This is not a new problem. Q1 2025 saw a $541.92 million negative MSR mark, and Q3 2025 carried a $264.35 million negative mark. The pattern is consistent: operating performance is solid; accounting volatility is relentless.

The Identity Tension

CEO Michael Nierenberg has been explicit about where he wants to take the company. On the Q4 earnings call, he said: “At some point, we will need to become a C-Corp and continue to grow our asset management business.” He even invoked Blackstone as a reference point: “Currently, our company has approximately $8.5 billion in permanent capital and generates over $1 billion in pretax earnings, trading at about 6 times earnings. Real asset management businesses typically trade between 10 to 30 times earnings.”

The gap between those multiples is the entire bull case. Rithm’s December 2025 acquisitions of Crestline Management ($18 billion AUM) and Paramount Group’s Class A office portfolio for roughly $1.6 billion pushed total investable assets past $100 billion. Sculptor Capital contributes approximately $38 billion in AUM. The asset management segment generated $403.2 million in Q4 revenue alone.

Yet the market still classifies Rithm as a mortgage REIT. The stock trades at 0.74x book value against a book value of $12.66 per share, while the current price sits near $9.11. The analyst consensus price target is $14.50, with 10 buy or strong-buy ratings and zero sells.

What the Market Is Pricing In

The stock is down 16.88% year-to-date and off 15.49% over the past year. The weekly RSI has fallen to 26.54, deeply into oversold territory. The dividend yield now stands at 10.7% on a $1.00 annual payout.

The skepticism likely reflects MSR volatility and the difficulty of valuing a company that is simultaneously a mortgage servicer, originator, credit manager, and commercial real estate owner-operator. Until Rithm converts to a C-Corp or demonstrates that asset management fees can structurally offset MSR swings, investors face a company priced like a REIT but pitching itself like an alternative asset manager. Nierenberg acknowledged as much: “Eventually, the company will be revalued, and we are eager to continue growing our business.” The question is how long that rerating takes.